Yes, travel has grinded to a halt yet again, what a great start to 2020 (2). Before COVID happened, well travelled Singaporeans flocked to The Arcade and Lucky Plaza to get their hands on cash for their desired holiday destination.

We also had the option of exchanging currency on Multi Currency Card accounts, then withdrawing them in cash overseas. The fees however, can be hefty for smaller withdrawals.

For most, the best option was to convert SGD to a supported currency, then using the Visa/Master card to pay for items directly in foreign currency.

But with travelling and spending foreign currency in person out of the picture, let’s take a look at how these Multi Currency Cards remain relevant today.

Why Multi Currency Cards?

There are two main fees to take note of that bank debit/credit cards charge when dealing with foreign currency and transactions processed outside of Singapore. Multi Currency Cards do not incur any of these fees.

The first fee is from when you transact in foreign currency. All banks operating in Singapore like UOB, DBS, OCBC levy this fee that can range from 2.8% to 3.25%.

What’s more, the SGD amount charged to your card is based on the exchange rate decided by your bank. And that will unlikely be the “Google” or “real” rate at the point of settlement.

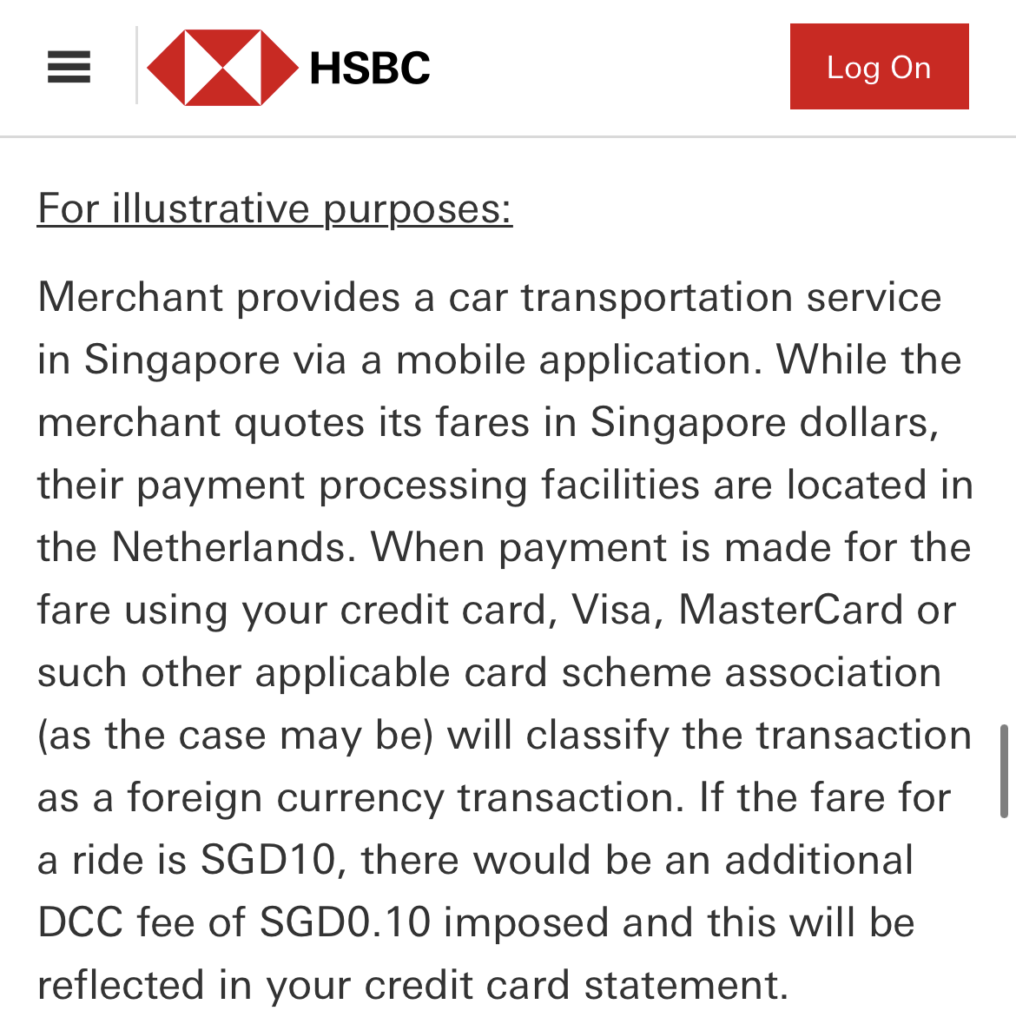

The second fee is from dynamic currency conversion. Have you ever paid your Spotify subscription and realised that you were being charged an extra 1%?

It can be baffling to see how your payment completed in Singapore, in Singapore dollars is charged a currency conversion fee.

In HSBC’s words, if the payment processor is not based in Singapore, a 1% fee is levied.

It’s quite hard to find out whether a payment you’re making is processed overseas or not. For instance, you would assume that Netflix, like Spotify would be subject to the DCC fee too.

Instead, Netflix has its own local payment processor and is not subject to DCC. Really, the only way to find out is by either trial and error, or by community sharing.

So for your TaoBao hauls (1% DCC levied) and random purchases in foreign currency (2.8% – 3.25% levied), it is better off to use a Multi Currency Card to pay for these.

This is especially true if you don’t earn any rewards from your debit card, or don’t have access to a rewards credit card.

Let’s take a look at the popular offerings in Singapore and see how they compare.

YouTrip

Youtrip is one of the first entrants into the Singapore Multi Currency Card market in 2018. What they offer is an EZ-Link enabled Master card that you can top up using another debit/credit card.

It’s quite funny how they collaborated with EZ-Link in 2018 to provide access to public transport, when Master cards were accepted as a payment source for public transport the very next year.

Anyway, here are the key features YouTrip brings to the table:

| Card Fee | First card free, subsequently S$10 per card |

| Top Up Fee | 1.5% for Visa Credit Card Top Ups, no fees for PayNow, Visa Debit Card, and Master |

| Foreign Currency Exchange Fee | None |

| Supported Currencies For Holding | SGD, USD, EUR, GBP, JPY, HKD, AUD, NZD, CHF, SEK |

| Overseas ATM Withdrawal Fee | S$5 per withdrawal |

| Currency Auto Conversion | Yes |

| Ability To Withdraw Funds To Local Bank Account | No |

While YouTrip only supports 10 currencies to be exchanged and held anytime at your preferred rate, they also support the auto conversion from SGD to 140 other currencies at the point of your purchase.

YouTrip uses Mastercard’s Wholesale Exchange Rates for all your currency exchanges, so the rates are as close to the “Google” or “real” rate as possible.

Don’t be shocked by the 1.5% Visa Credit Card top up fee though. This is due to a new fee structure introduced to Visa credit cards, and many E-wallets like GrabPay also charge similar fees.

One thing to note, YouTrip does not support SGD withdrawals back to your bank account or local ATM withdrawals. So make sure the amount you top up is exactly what you need to avoid having leftover funds in your wallet.

However, by using the YouTrip card to top up the GrabPay card (minimum S$20), you are able to withdraw the balance in the Grab app (working as of 2 Jan 2022).

If you are interested in signing up for YouTrip, use my link here for free S$5 once you sign up, order a card, and make your first top up.

Revolut

Next, we got Revolut, a Fintech Unicorn founded in London. They entered Singapore’s market back in October 2019, almost a year later than YouTrip did.

Revolut boasts not just one, but 3 types of Multi Currency Cards:

The Physical one works like any other Visa card.

The Virtual Card only exists on your Revolut app for online and mobile payments.

The Disposable Virtual Card works exactly like a Virtual card, but its card details are changed after every transaction.

Revolut’s card features are as follows, assuming you are on the free plan:

| Card Fee | First card free, subsequently S$9 per card |

| Top Up Fee | None |

| Foreign Currency Exchange Fee | 0.5% after monthly S$5000 limit is used, 0% for most currencies, but 1 – 2% outside of foreign exchange market hours (terms) |

| Supported Currencies For Holding | AED, AUD, BGN, CAD, CHF, CZK, DKK, EUR, GBP, HKD, HRK, HUF, ILS, JPY, MXN, NOK, NZD, PLN, QAR, RON, RUB, SAR, SEK, SGD, THB, TRY, USD, ZAR |

| Overseas ATM Withdrawal Fee | Free for first S$350 per month, 2% on subsequently |

| Currency Auto Conversion | Yes |

| Ability To Withdraw Funds To Local Bank Account | Yes |

Revolut uses independent sources and market data feed to determine the exchange rate of currencies that can be viewed here. Rates are determined at the point of purchase if you do not have sufficient foreign currency in your wallet.

Based on my experience, the rates are almost the same as Visa or Master’s Wholesale Exchange rates if exchanged on a weekday.

Unlike Grab and YouTrip, Revolut doesn’t charge anything for card top ups, even Visa credit cards.

So if you want to pay the card top up for foreign currency purchase together with your Visa credit card bill later in the month, you can certainly do it for free.

Revolut’s foreign currency exchange is available for major currencies for free, up to S$5000 per month unlike YouTrip’s unlimited free exchanges.

But if you sign up for their Metal plan which costs S$19.99 per month, you get unlimited free exchanges. Note that weekend markups still apply.

One unique feature about Revolut, is that you are able to withdraw the currencies in your wallet, be it SGD or any of 28 currencies listed above.

SGD withdrawals are free and instant, while foreign currency transfers start from S$0.30. The price list can be found here.

Revolut supports Apple Pay and Google Pay, so you can easily check out online using either one of your cards with just a click.

Wise

Wise, formerly known as TransferWise entered Singapore’s remittance market in April 2017, but has since ventured into the Multi Currency Card market since.

Unlike YouTrip and Revolut, Wise does not provide a free debit card upon sign up. S$10 is charged instead.

The key features are as follows:

| Card Fee | S$10 |

| Top Up Fee | None |

| Foreign Currency Exchange Fee | Small currency conversion fee from 0.35%, exchange uses the real mid-market exchange rate |

| Supported Currencies For Holding | 56 currencies |

| Overseas ATM Withdrawal Fee | First 2 withdrawals free to a maximum of S$350 per month. 1.75% fee + S$1.50/withdrawal subsequently |

| Currency Auto Conversion | Yes, but from 0.35% each time |

| Ability To Withdraw Funds To Local Bank Account | Yes |

Yup, clearly, the 0.35% starting fee on all foreign currency exchanges does not bode well with consumers after seeing Revolut and YouTrip’s offerings.

The mid-market exchange rate is very close to the rest of the competition, but the fee will eat away at some potential savings.

But like Revolut, Wise offers zero fee top ups regardless of payment method, and provides free ATM withdrawals up to S$350.

As Wise’s main business is money remittance, SGD and foreign currencies exchanged can also be withdrawn to external bank accounts.

However, all withdrawals are subject to a fee, even SGD. The fees can be calculated here.

Instarem Amaze

Next up, Amaze by Instarem. Like Wise, Instarem is a money remittance company that started to venture into the Multi Currency Card market in 2021 by introducing the Amaze card.

The Amaze card works drastically different from YouTrip, Revolut, and Wise cards. Instead of having to top up a balance and holding foreign currency, the Amaze card directly debits the SGD equivalent of the foreign currency purchase from your Mastercard.

Amaze’s exchange rates are very close to ones by Visa and Master, so you don’t have to worry about paying extra. MoneySmart did a few purchases to illustrate this. Do check them out.

Here’s the thing, on top of saving on the 1% DCC or 2.8% – 3.25% foreign exchange fee, you get your usual card rewards based on the charged SGD amount. Best of both worlds.

To sweeten the deal even further, Amaze provides an additional 1% cashback capped at S$100 per quarter credited to your Instarem wallet.

This is for purchases above S$5, given a minimum quarterly spend of S$500.

It easily trumps all the aforementioned Multi Currency Cards in terms of value. However, Amaze only supports the linking of Master cards. So favourites like HSBC Revolution, DBS Altitude or UOB Preferred Platinum Visa cannot be used with Amaze.

If you’re just looking for a card for quick foreign currency purchases without the ability to exchange, hold and withdraw currencies, Amaze is an (pun intended) amazing value.

Conclusion

Now for avid online shoppers, the choice of using a Multi Currency Card or a regular bank card depends on the amount of value you are getting.

If you don’t have access to a credit card and are using a basic debit card with around 1% in rewards, it is a no-brainer to use a Multi Currency Card for foreign currency purchases and purchases processed overseas to save the 2.8% – 3.25% fee.

But if you are already using a credit card that provides more than 2.8% – 3.25% in rewards, paying the Foreign Currency Exchange Fee may still be worth it overall.

And if the credit card you own is a Mastercard, link it to Amaze to get the best of both worlds: rewards and avoiding the Foreign Currency Exchange fee (don’t know how long this will last).

Otherwise for the vast majority of us, Revolut and Youtrip are great picks for related purchases depending on which currency you’d like to exchange and hold. Wise just doesn’t seem as competitive as the others in terms of its fees.

This article may include Referral or affiliate links that provide revenue to Tech Composition.

Derrick (Yip Hern) founded Tech Composition to provide valuable insights into the tech and finance world. He loves to scour the web for the best deals and embark on software projects during his free time, a typical geek, right?

Thank you very much for sharing, I learned a lot from your article. Very cool. Thanks.